How do payments work at casinos not on GamStop?

By , iGaming Regulation and Self-Exclusion Analyst — — 9 min read

Payments are where non-GamStop casinos look most different from anything you will find at a UK-licensed site, and where the differences carry the most risk. These operators lean heavily on cryptocurrency, lean on a wider spread of e-wallets and vouchers, and sometimes accept payment types that a British casino is forbidden to touch. This page answers the practical question of how money actually moves in and out of these sites, while being honest that several of the methods on offer are risk markers in their own right rather than the conveniences they are sold as.

What payment methods do these sites actually use?

The payment menu at an offshore site is broader and looser than at a UK casino. Cryptocurrency is the headline option, and many sites are built around it. Beyond crypto you will typically see debit and credit cards, e-wallets and a range of prepaid vouchers. Some of these are familiar from the UK market; others exist precisely because they sidestep the banking system that would otherwise refuse the transaction.

Cryptocurrency

Bitcoin, Ethereum and the stablecoin USDT are the most common, with some sites adding others such as Solana. Crypto is the rail that makes much of the offshore model work, because it does not need a bank or card network to approve the transfer.

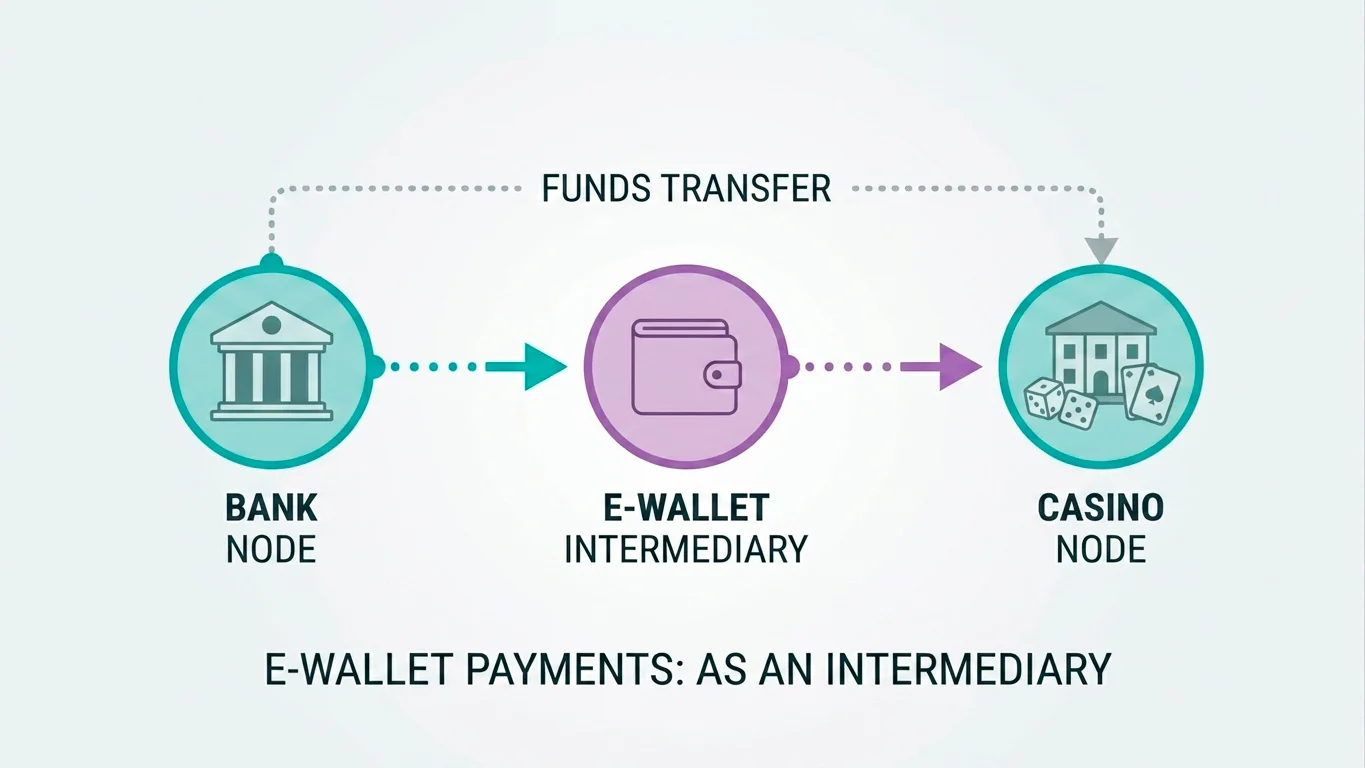

E-wallets

Skrill, Neteller and Payz appear frequently. They can be quick, but they are sometimes excluded from bonus eligibility and still rely on you funding them from a bank or card.

Prepaid vouchers

Paysafecard, Neosurf and CashtoCode let a player deposit without a bank link. They are deposit-only, capped at modest amounts, and offer no route for a withdrawal.

Cards

Debit cards may work; the appearance of credit-card acceptance is a warning sign for reasons covered below.

E-wallets sit in an awkward middle ground. They are quick and they add a buffer between the casino and your bank account, which some players value, but they do not change the underlying picture: the money still starts in a bank or on a card, and the wallet provider has its own rules about gambling that can see a transaction declined. Several operators also quietly exclude e-wallet deposits from bonus eligibility, so a deposit that qualifies you for a welcome offer by card may not qualify by Skrill or Neteller.

Prepaid vouchers are the most limited option and, for some, the most telling. Because they let a player top up without any bank link at all, they are attractive precisely to people who want their gambling to leave no trace on a statement — which can include people who have asked their bank to block it. They are capped at small amounts and cannot be used to withdraw, so they are a deposit funnel rather than a real payment relationship. For the bigger picture of which operators offer which methods and why the licence shapes the payment menu, the non-GamStop operator overview is the place to start.

Why is credit-card acceptance a warning sign?

One of the clearest UK signals sits in what a site lets you pay with. Credit cards have been banned for gambling in Britain since April 2020, across Visa, Mastercard and Amex credit products. The ban was introduced specifically to stop people gambling with borrowed money they did not have, and it applies to every UK-licensed operator without exception.

So if an offshore casino happily takes your credit card, it is not offering you a convenience that British sites are too stuffy to provide. It is demonstrating that it operates outside the rule designed to protect you from gambling on credit, which tells you something about how seriously it takes player protection generally. Treat credit-card acceptance as a red flag, not a feature. The government’s policy background on payment and gambling rules sits on GOV.UK, and the regulator’s payment-services conditions are published by the UK Gambling Commission.

Will a UK bank block these payments?

It often will. Many UK banks now offer a gambling block, a free setting that lets a customer stop their account being used for gambling transactions, and these blocks are commonly used by people who have stepped away from gambling deliberately. Even without a block in place, a bank may decline or flag a transfer to an unlicensed gambling operator as part of its own fraud and risk controls.

This is why crypto and vouchers feature so heavily on offshore sites: they route around the bank. A player whose card payment is declined is nudged towards a method the bank cannot see or stop, which is convenient for the operator and removes a safeguard for the player. If you have a gambling block switched on, that block exists for a reason, and a site that helps you get around it is not acting in your interest. The page on fund security and payout risks looks at what happens when those safeguards are gone.

Is crypto a convenience or a risk?

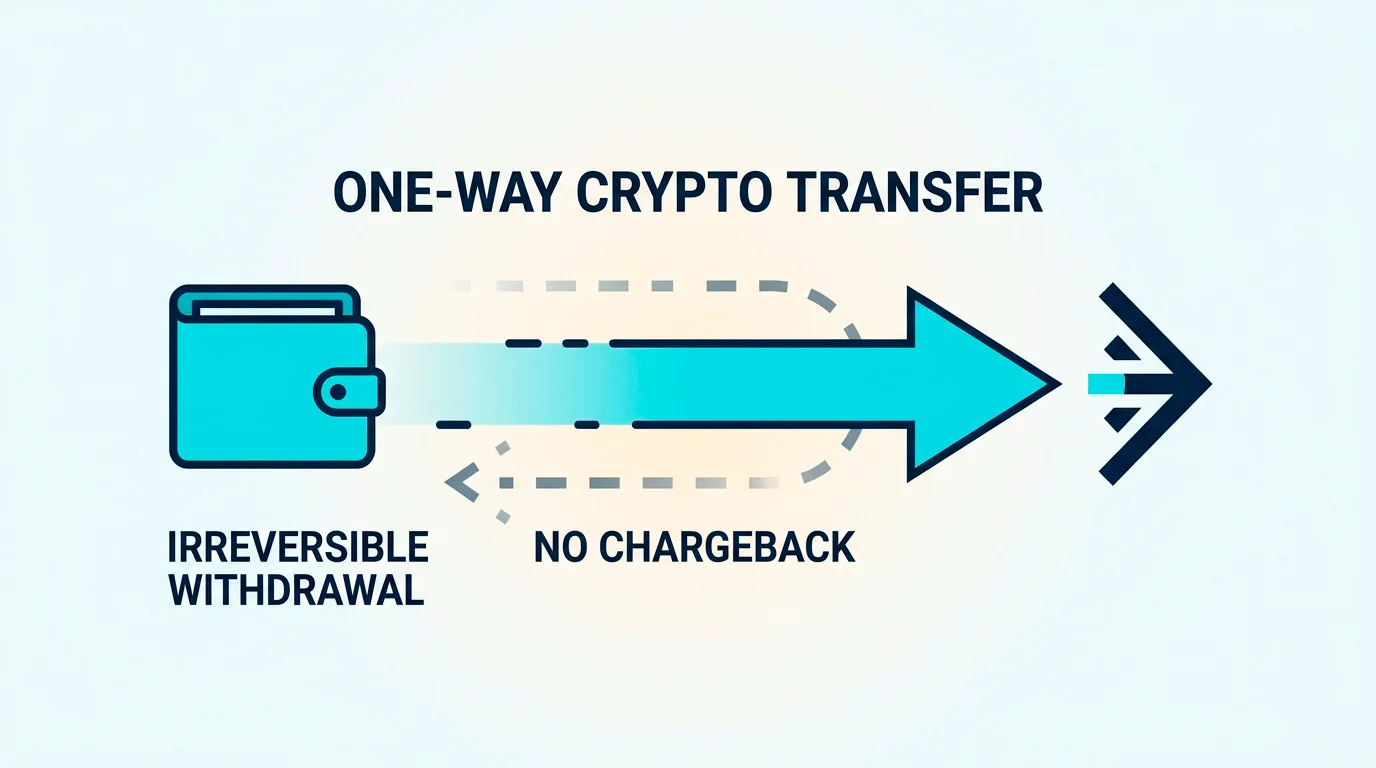

Both, and it matters which one you are weighing. On the way in, crypto is genuinely fast and frictionless. On the way out, the same properties that make it quick also strip away every protection you might later wish you had. There are no chargebacks, transfers are irreversible, and there is no payment provider standing between you and the operator to intervene if a withdrawal stalls or a balance is voided.

There is also volatility. If you deposit in Bitcoin and the price moves before you withdraw, the value of your balance can shift independently of how you played, which is a risk that simply does not exist when you deposit in pounds at a UK site. And because crypto is the method of choice for low-verification operators, it tends to travel with the deferred-KYC problem: the site that took your crypto instantly may still demand documents before it releases your winnings. That overlap is covered on the page about low-KYC sign-up and the catch. For context, the UK and its regulators are still cautious here; a consultation in February 2026 looked at whether licensed operators might accept crypto, and it remains not permitted at retail level, which is one more reason offshore crypto sits entirely outside UK payment protections.

What does the deposit and withdrawal flow look like in practice?

Stripped of the marketing, the mechanics are simple enough. A deposit by crypto means sending coins from your own wallet or an exchange to a wallet address the casino gives you; it usually credits within minutes once the network confirms it. A deposit by e-wallet or voucher is near-instant. Card and bank deposits, where accepted, behave much as they would anywhere, subject to the bank actually allowing the transfer.

Withdrawals are where the experience diverges. Crypto withdrawals can be fast, sometimes within hours, which is the selling point — but that speed depends entirely on the operator approving the payout, and approval is where verification and source-of-funds checks reappear. It is worth being clear-eyed about this: a fast withdrawal method is not the same as a fast withdrawal. The rail can move money in minutes, but only after a human or a system at the casino has decided to release it, and an offshore operator faces no UK deadline forcing it to do so. For a sense of how the new British regime contrasts with all of this, the comparison with UK-licensed sites in the breakdown of bonuses and wagering terms shows how differently the two markets treat the money attached to a sign-up. On a UK site, for contrast, the dominant methods are Visa debit and Apple Pay, both of which keep you inside a regulated payment chain with recognised recourse if something goes wrong. The convenience offshore is real, but it is bought by stepping outside that chain, and the main guide to casinos not on GamStop sets out the full set of trade-offs that come with it.

Support and safer-gambling tools

This page explains how payments work; it does not encourage anyone to fund gambling that is causing harm. If you have a bank gambling block in place, or you have self-excluded, please treat those tools as the protection they are. Free, confidential help is available across the UK at any hour. The National Gambling Helpline, run by GamCare, is on 0808 8020 133, free and open 24 hours a day, every day. You can also find prevention and support resources through GambleAware, and free blocking software through the TalkBanStop partnership.

About the author

Owen Radcliffe has spent over twelve years tracking the UK online gambling market, with a particular focus on licensing, self-exclusion frameworks and the offshore operators that sit outside the GamStop scheme. He writes plain-language analysis aimed at helping readers understand the regulatory and financial trade-offs before they act. More about Owen Radcliffe.